Scary Times in the Skies

The state of US airlines in 2020

This week, we’re doing a vitals check on the airline industry: who’s still flying, who’s cutting employees like Edward Scissorhands, and who’s looking for a multibillion favor. To help, we’ll also look at the profit structure of a typical airline, which blew my mind.

Turbulence

Anywhere you look, the data tells the same story about US airlines. Months of Coronavirus-fueled anxiety brought air travel to a screeching halt, leaving each US airline on life support.

No major US airline has yet succumbed to the crushing weight of profit loss and flight-avoidance, due solely to the fact that President Trump signed a $25 billion aid package into law.

This bailout was created six months ago, in hopes that the travel industry would be back on its feet come Fall. The aid was stipulated with a conditional ban on layoffs, which happened to expire October 1st.

How bad is it?

Through the last several weeks of October, American Airlines has commenced a flow-controlled scything of 19,000 employees, while United has followed suit with plans to release 13,000.

What about the other major US airlines?

Southwest: No furloughs in 2020 yet, but CEO Gary Kelly warns of looming layoffs if no future aid is offered.

Delta: No layoffs yet due to budget cuts, early retirements, and buyouts. Similar impending-doom statements offered as Southwest.

JetBlue: A pilot’s union agreement has prevented involuntary furloughs until April of 2021. We’ll see how the rest of the workforce fairs.

Congressional Roadblocks (Surprise Surprise)

The fate of US airlines and their hundreds of thousands of comprising employees rests in the slippery, undexterous hands of Congress. While there is widespread support for another $25 billion in aid to airlines, the help train got derailed by disagreements on the larger pandemic-relief picture.

With hotels, restaurants, and retail still struggling, the general sentiment in Congress is against buoying a single industry. Thus, everyone treads water in shark-infested waters while Congress squabbles.

THE GRAPHS

A decent article from Road Work Ahead would be nothing without some graphs to aid your understanding of the situation. Despite my relative distaste for my degree in Math, I’m a sucker for some good data visualizations.

The following graph is from the Bureau of Transportation Statistics (BTS), showing US airline traffic data from this June.

That’s a voluptuous graph if I’ve ever seen one.

February through May of 2020 lent new meaning to the word “dip”, as monthly passengers on US scheduled airlines plummeted from ~65 million to a meager 2 million.

Here’s an additional visual aid:

In August, the picture was largely just as ugly, with slight improvements:

April saw a nearly 100% decline in air traffic from the levels of the corresponding time in 2019. Wild. By August, traffic had increased slightly to represent a 70% decline from August of 2019.

Unfortunately, I’m not able to find more recent info. The BTS has a report for September’s airline traffic to be released in December, which isn’t exactly helpful.

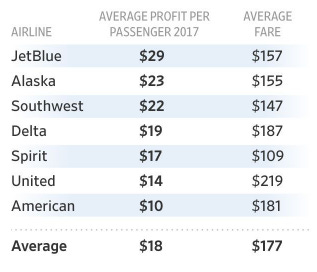

Airline Profit Structure

A report from the Wall Street Journal queries, “How Much of Your $355 Ticket is Profit for Airlines?” I’ve often wondered about this. I assumed that considerably high ticket prices must mean high profit margins for airlines.

Think again.

In 2018, the average profit per passenger among US airlines was $19.65. Just 20 bucks. That $355 gets distilled and siphoned off to the multitude of expenses that airlines face until $20 remains that an airline can pocket.

What’s more, 2018’s profit margins were record highs among airlines worldwide. In 2017, the average profit per passenger was $17.75. This profit was reached after 17 straight quarters of positive growth among airlines, meaning that 4 years before, profits were significantly lower.

Keeping $20 per passenger is roughly twice the profit recorded by airlines outside the United States, according to data from the International Air Transport Association.

According to the Wall Street Journal, airlines cover the expense of each flight through ticket fees, and only rake in profits through baggage fees, seat fees, and reservation-change fees. In fact, US airlines were on track to collect $4 billion in baggage fees and $3 billion in reservation-change and cancellation fees in 2017 alone.

United Airlines charging $40 just to bring a carry-on makes way more sense now.

Delicate, Expensive Chunks of Metal

Airlines have been in trouble before. Since 2000, Delta, United, and American have all declared bankruptcy at one point, and only survived by merging with other airlines.

So what makes airlines such a fragile industry?

Besides airplane leases, maintenance costs, and salaries, much of an airline’s expense comes from the price of oil. If oil prices are high, profit margins are squeezed. If low, the belt loosens and airlines achieve the profitability of average American businesses.

The historic volatility of oil markets is intrinsically tied to the welfare of airlines, and brings the entire industry along for whatever whiplash ride it decides to take.

In April, the price of oil went negative for the first time in history. Yup, negative.

Oil companies were literally paying people to take barrels of oil. Sounds like a mashup of Oprah Winfrey and Mad Max that no one asked for.

Due to global travel lockdowns at the beginning of the pandemic, demand for oil completely dried up. Worried that storage capacity would be surpassed, oil companies offered to pay ~$35 along with your complimentary barrel.

If this had happened at a time where air travel wasn’t reduced by 96%, flights could have been cheap, and airlines could have remained profitable.

Point being, airlines are beholden to volatile industries they have no control over, and this makes them inherently risky.

The Future of Airlines

As the pandemic continues, airline use will remain deprecated.

A significant and profitable arm of the airline industry was held by business travel. Airline profits are heavily influenced by the First and Business Class seats, where extra fees help pad the balance sheets.

With business travel all but stopped and the adoption of Zoom widespread, it’s hard to see business travel regaining the levels it once had.

In a meeting between airline executives held in April, fully 44% of the representatives believed it would take 18 months to 3 years for airlines to fully recover. Another 30% believed it would take even longer.

Without significant action by the government, airlines will continue to hemorrhage employees, pilots, and planes. Recent spikes in Coronavirus across the world certainly paint a bleak picture for air travel as the threat of lockdown once again looms large.

I’m eager to see how Congress and the impending election will handle the need for aid across multiple industries - stay tuned for more!

If you know someone who would benefit from these weekly newsletters, click below to share with them!

Thanks for reading :)